Wasde preview: US wheat teed up, but Black Sea remains the focus

The July update of the USDA’s influential World Agriculture Supply and Demand Estimates will lift the lid on the profile of the US’s 2022/23 wheat crop, but once again the focus is likely to be on the Black Sea and the continuing agony of Russia’s invasion of Ukraine.

With the EU, Ukraine and Russia all entering new marketing years, production is starting to reach the crunch point across the region – although this year, mere output is only part of the equation and access to the sinews of export will be vital.

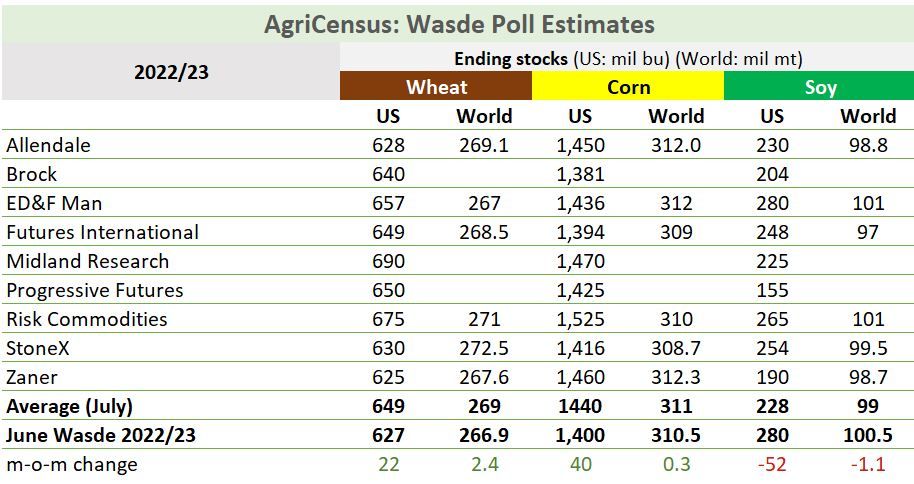

Starting with headline US figures, an Agricensus survey of analysts reflected updated expectations in light of the quarterly stocks and planting report with old crop ending stocks nudging higher after high prices dampened demand.

For new crop 2022/23 ending stocks, analysts also looked for an increase versus last month’s figures with an on average increase of 22 million bushels (600,000 mt) taking US stocks to 649 million bu (17.6 million mt).

Globally, though, analysts polled are looking for new marketing year stocks to continue to rise – up 2.4 million mt on average to 269 million mt.

That increase markedly outpaces the build in US stocks and suggests that much of that increase is likely to come in the Black Sea, where Russian forces continue to blockade Ukraine’s export capacity as their invasion approaches the six-month mark.

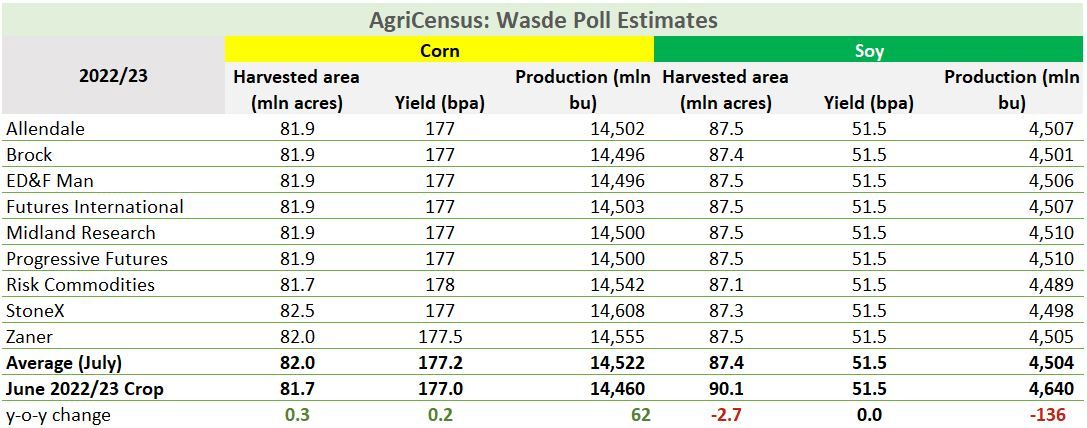

Turning to the complexion of the new US crop, analysts are – unsurprisingly – still looking for production to increase year-on-year, with average guesses calling for 1.7 billion bu (47.8 million mt), up 111 million bu (3 million mt) versus current 2021/22 outlooks.

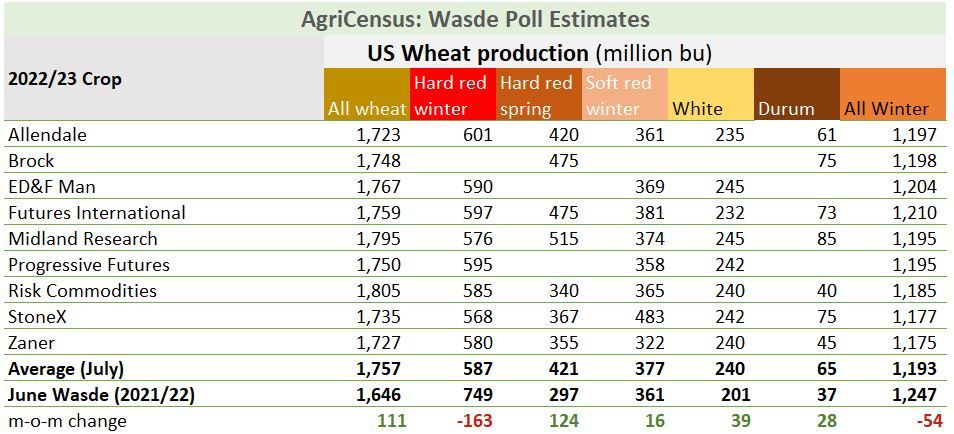

July will bring the first by-class projections for the new marketing year, but analysts are looking for a major year-on-year reduction in hard red winter production, down 163 million bu to 587 million bu on average (16 million mt).

Every other class is expected to post an increase though, with hard red spring leading the charge with a near 41% uptick expected to bring output to 421 million bu (11.5 million mt).

Soft red winter is expected to weigh in at 377 million bu, with durum also up substantially to 65 million bu – a 75% increase versus 2021/22.

Black Sea

Beyond the US figures, the focus will remain on the Black Sea – although Argentina, India and Australia will also likely be watched.

With India’s output standing at 106 million mt, down 2.5 million mt at last month’s update, changes are not expected this month.

Much the same could be said for Australia, where dry conditions have capped some of the early optimism and make 30 million mt a decent figure for the current conditions, while Argentina lacks any major fresh inputs to depose the current 20 million mt forecast.

But the Black Sea remains the engine-room capable of driving prices.

The US agency has already put its Ukraine production estimate at 21.5 million mt, broadly in line with local expectations, but exports remain set at 10 million mt.

A flurry of investment proposals and support to the Ukrainian infrastructure could yet move that figure higher, but for now prospects of any improvements in export figures remain remote and the greater risk remains to the downside and a fresh build in stocks – currently at 6 million mt.

Which leaves Russia as the big unknown.

Local estimates are markedly out of whack with the USDA’s current thinking of 81 million mt, versus estimates of up to 87 million to even 90 million mt.

The USDA added a million tonnes to its production and export estimate at the last update, but with production likely to spiral higher there will be strong consideration of an increase on both values – with Russian exports also potentially bolstered by further thefts of Ukrainian grain.

All that is underpinned by an increase in the planted area and an increase in yields of up to 6% year-on-year.

The USDA will release its July 2022 Wasde report at 1200 Eastern Time on July 12.